Nifty 50 vs S&P 500: Valuation, Performance, and Outlook (2026)

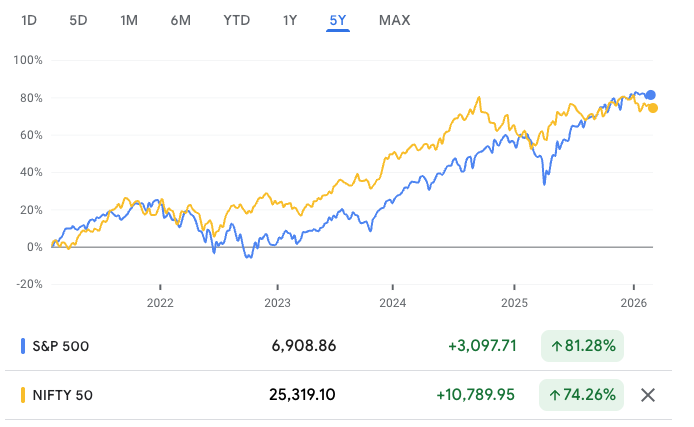

As of February 2026, Indian and US equity markets are trading at interesting levels of valuation and momentum. The Nifty 50 sits at a trailing price‑to‑earnings (PE) ratio of around 22.03x, while the S&P 500 trades close to 24.75x. India has delivered relatively muted returns compared with the US over the past few years. This gap reflects a mix of earnings growth, sector composition, currency dynamics, and global‑risk sentiment that shapes how both indices perform and what investors can reasonably expect in the coming years.

Valuation snapshot: Nifty versus S&P 500

Valuation metrics are the first lens to compare Nifty and the S&P 500. As of early 2026:

Nifty is clearly cheaper than the S&P 500 on both PE and P/B, but it is still at premium versus its own long‑term average and other emerging‑market peers. Over the last decade, Indian equities were bid up on expectations of strong GDP growth, corporate‑earnings expansion, and structural reforms, which pushed multiples into the low‑20s. In contrast, the S&P 500 sits at one of the highest PE levels in its post‑2008 history, reflecting a heavy skew toward large‑cap tech and AI‑related names that are assumed to grow earnings at a faster pace.

| Metric | Nifty 50 (approx.) | S&P 500 (approx.) |

|---|---|---|

| Index level | ~25200 – 25500 | ~6800 – 6950 |

| PE (TTM) | 22.03x | 24.75x |

| Forward PE (est.) | 20–21x | 21.5–22x |

| P/B ratio | ~3.4–3.5x | ~5.5–6.0x |

| Dividend yield | ~1.2–1.3% | ~1.14–1.16% |

| 5‑year CAGR (price) | ~12–13% (INR‑terms) | ~13–14% (USD‑terms) |

Despite the S&P 500’s premium valuation, its total‑return performance has been stronger than Nifty’s over 2023–2025, especially when returns are measured in US dollars. For dollar‑based investors, Nifty’s rupee‑denominated gains were partly offset by rupee depreciation. As a result, the attractiveness of Indian equities in global portfolios is affected negatively.

Why Nifty underperformed in 2023–2025

Several factors explain why Nifty has lagged the S&P 500 and many global indices in recent years.

1. Valuation reset after a long bull run

From 2020 onwards, Indian equities priced in very optimistic growth expectations, taking Nifty’s PE to the range of 27 – 29 in 2021. This created a premium over many emerging‑market peers. When earnings growth slowed to around 5–6% in 2025, instead of the mid‑teens many had anticipated, the market had to compress valuations. This led to a flattening of the index’s trajectory and weaker relative performance versus the US‑driven global rally.

2. Missed AI‑led US tech rally

The S&P 500’s outperformance in 2023–2025 was driven largely by the “Magnificent 7” and AI‑themed tech stocks, sectors where India has limited representation in the Nifty. The rise of cloud computing, artificial intelligence, and data‑centric infrastructure boosted US‑listed mega‑caps, while Nifty’s composition is more tilted toward financials, energy, and consumer staples. These sectors benefited less from that specific growth wave, which widened the performance gap.

3. Currency and foreign‑inflow headwinds

The rupee weakened sharply in 2025, briefly touching levels above ₹90 per dollar, turning India’s mid‑teens rupee‑denominated returns into low single digit returns for dollar‑based investors. At the same time, geopolitical friction over India‑linked Russian‑oil trade and US‑India tariff disputes created uncertainty for foreign investors, leading to net outflows from Indian equities. This combination of currency drag and fading foreign‑investor sentiment weighed on Nifty even as the underlying economy and corporate balance sheets remained relatively healthy.

4. Policy and expectations gap

Expectations around India’s reform agenda, including tax simplification, infrastructure‑capex continuity, and governance standards, often ran ahead of visible delivery. Meanwhile, the India–US trade accord was delayed until 2026, keeping sectors like IT and manufacturing in a wait and see mode and limiting the kind of export‑related growth that could have lifted the index more decisively. Analysts have described this period as one where valuations were high but earnings growth was only moderate, creating a “valuation‑earnings” mismatch that dampened investor appetite.

IT sector collapse: The recent AI revolution have affected Indian IT industry very badly with NIFTYIT falling by around 20% in February 2026 (worst since 2003), wiping ₹6.4 lakh crore; stocks like Infosys (-35%), TCS (-41%), Wipro (-44%) down from their all time highs, hit hard by AI automation fears disrupting service models. IT stocks have 8.84% weightage in the Nifty.

Correlation and volatility: risk‑return trade‑off

Historically, the correlation between Nifty and S&P 500 is only modest, and in some periods it has even turned negative when measured in common currency. One investor‑level study found a correlation of roughly –0.35 when converting the S&P 500 into rupee terms, implying that the two indices sometimes move in opposite directions over measured windows.

Key volatility characteristics (roughly 26th Feb 2021– 27th Feb 2026) are:

- Nifty: 11.5% annualized, reflecting the combination of earnings‑sensitivity and rupee fluctuations.

- S&P 500: 12.5% annualized, reflecting global‑risk sentiment and the impact of large‑cap tech and cyclical names.

For a diversified portfolio, this mix of modest correlation and differing volatility profiles means that holding both indices can help spread risk, especially if investors hedge currency exposure or use dollar‑hedged Indian ETFs to smooth returns.

What to expect going forward

Looking ahead, several trends will shape the relative performance of Nifty and the S&P 500.

For India, the key determinants are:

- Whether Nifty earnings growth can accelerate PE towards 23 to 25 in FY26–FY27, it might find the support at current levels and justify a higher index level.

- The stability of the rupee and the return of foreign‑investor interest, especially if India‑US trade and India‑EU trade pacts lead to stronger export‑linked earnings in sectors like IT, manufacturing, and autos.

- Continuity in domestic reforms and infrastructure spending, which can sustain the structural‑growth story that has underpinned India’s premium valuation.

For the US, the main drivers are:

- The pace of AI‑driven earnings growth and whether the S&P 500’s rich valuation can be justified by sustained profit expansion in technology and related sectors.

- Interest‑rate and macro‑policy decisions from the Federal Reserve, which can amplify or compress multiples across the entire index.

- Global‑risk sentiment, which often flows through the S&P 500 as a proxy for “global risk‑on” or “risk‑off” positioning.

Many analysts and banks project Nifty to move toward a 28,000–30,000 band by end‑2026 under a base‑case scenario of moderate earnings growth, stable macro conditions, and no major external shocks, implying low‑ to mid‑teens compounded returns. The S&P 500 will go up higher as well, but with a higher valuation cushion and stronger link to global‑tech cycles, which can create both upside and fragility in a shock‑prone environment.

What it means for investors

For a long‑term investor, the takeaway is that Nifty offers growth at a moderate premium, while the S&P 500 offers global‑tech‑driven growth at a rich premium. Allocation between the two should reflect. In Indian Stock markets, many largecaps are currently a good investment opportunity for long term investors. But SIPs should be the way rather than investing a big lumpsum into the Mutual Funds and Stocks.

- Currency risk tolerance (how much exposure you want to rupee moves vs stable‑dollar returns),

- Sector tilt preferences (financials, energy, and consumption vs tech and AI),

- Valuation comfort (22x PE vs 30x PE).

For a trader or options‑oriented investor, the key is to watch:

- Earnings guidance and sector‑earnings surprises in both markets,

- Macro‑policy shifts (US Fed and India’s central bank), and

- Trade‑related news around India–US and India–EU agreements that can tilt sentiment toward or away from India.

References:

- https://www.wsj.com/market-data/stocks/peyields

- https://archives.nseindia.com/content/indices/ind_nifty50.pdf

Disclaimer:

I provide the information and my views on the website only to educate people, new investors, and stock market enthusiasts on equity and other market investments. Please consult a SEBI registered financial advisor before making any investments in the stock or commodity markets. In case of any queries, you can contact me on Contact Form or email: admin@valueinvestingonline.in.